I Ran the Numbers on a $400K Mortgage. Here's What You Actually Pay.

$320,000 borrowed. $446,428 paid in interest. $40 every single day for 30 years. We checked the math three different ways. Here's the breakdown most calculators quietly hide.

You're shopping for a $400,000 home. Your real estate agent says the monthly payment is "about $2,100." Your loan officer pre-approves you. Bankrate's calculator confirms the number. So you sign, you move in, and you tell yourself this is a good investment.

Then someone shows you the amortization schedule.

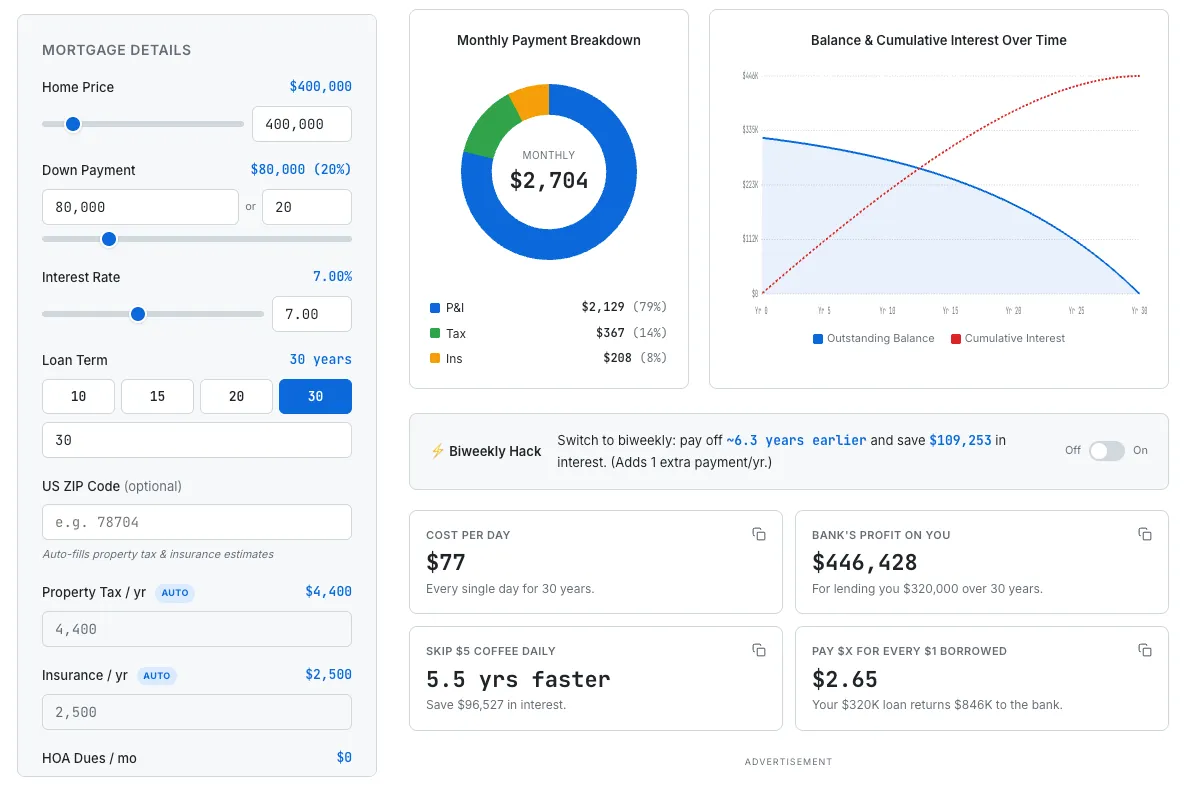

On a 30-year fixed mortgage at 7% — the rate that defined home buying through most of 2024 and 2025 — a $320,000 loan (the standard 20% down on $400K) costs you $446,428.47 in interest alone. Your bank gets back $2.40 for every $1 you borrowed. The first month of every payment is 87.7% interest. You don't pay more principal than interest in a single payment until Year 21.

And that's just the loan. Add property tax, insurance, maintenance, and one new roof, and the true 30-year cost of "owning" your $400K home approaches $1.4 million.

This isn't a gotcha post. The math is real. Your mortgage might be the right financial choice anyway. But you should see what you're actually agreeing to before you sign.

The Math, in One Box

The full breakdown:

| Metric | Value |

|---|---|

| Home price | $400,000 |

| Down payment (20%) | $80,000 |

| Loan amount | $320,000 |

| Interest rate | 7.00% |

| Term | 30 years |

| Monthly P&I payment | $2,128.97 |

| Total interest paid | $446,428.47 |

| Total payments (interest + principal) | $766,428.47 |

| Cost-to-home-price ratio | 1.92× |

| For every $1 borrowed, you pay back | $2.40 |

| Average daily interest cost | $40.77 |

Verify it yourself in any amortization calculator. The numbers are mathematically exact for fixed-rate loans — they don't change, they don't depend on assumptions. This is what you signed up for.

Your First Mortgage Payment Is 87.7% Interest

The brutal truth of amortization is the front-load. Every fixed-rate mortgage is structured so that early payments are mostly interest and late payments are mostly principal. On a $320,000 loan at 7%, your first month works out like this:

- Total payment: $2,128.97

- Interest portion: $1,866.67 (87.7%)

- Principal portion: $262.30 (12.3%)

You wrote a check for $2,128.97. Your loan balance dropped by $262.30. The other $1,866.67 went straight to your bank.

It gets worse before it gets better. Here's how the principal-vs-interest split evolves across the loan:

| Year | Monthly interest | Monthly principal | Loan balance |

|---|---|---|---|

| 1 | $1,849 | $280 | $316,749 |

| 5 | $1,759 | $370 | $301,221 |

| 10 | $1,605 | $524 | $274,600 |

| 15 | $1,386 | $743 | $236,860 |

| 17 | $1,275 | $854 | $217,669 |

| 20 | $1,076 | $1,053 | $183,360 |

| 21 (crossover) | $1,000 | $1,129 | $170,232 |

| 25 | $636 | $1,493 | $107,517 |

| 30 (final) | $12 | $2,117 | $0 |

The first month you pay more principal than interest is month 242 — early in Year 21. Until then, every payment is mostly rent paid to the bank for the privilege of staying in your house. The math is the same compound interest that powers retirement accounts — only this time it's working against you, not for you.

That $2,129 Monthly Payment Is a Lie

Most basic mortgage calculators show only P&I — principal and interest. Real homeowners pay PITI: Principal, Interest, Taxes, Insurance. Often plus PMI and HOA. Here's the gap:

| Component | Monthly | Annual |

|---|---|---|

| Principal & Interest | $2,129 | $25,548 |

| Property tax (national average ~1%) | $333 | $4,000 |

| Homeowners insurance (Bankrate avg, $300K dwelling) | $208 | $2,490 |

| PMI | $0 | $0 |

| True PITI | $2,670 | $32,038 |

| Gap vs P&I-only | +$541 (+25%) | +$6,490 |

That $541 monthly gap might sound small. Across 30 years it's $194,400 in additional housing costs that the calculator never showed you. And it gets worse over time, because property tax and insurance both rise:

- Property tax: The 2025 ATTOM report showed the average single-family property tax bill rose 3% year over year to $4,427. That growth compounds — over 30 years, your $4,000 tax bill becomes ~$9,700 (at 3% annual growth).

- Homeowners insurance: American homeowners faced a 24% increase over the past 3 years per the Consumer Federation of America. S&P Global Market Intelligence reports double-digit annual increases — 12.7% in 2023 and 10.4% in 2024. Florida averages between $7,000 and $10,000+ annually depending on the source. California rates are projected to rise another 16% in 2026 (Insurify).

Your "fixed-rate" mortgage isn't really fixed. The smallest portion of it is.

The True 30-Year Cost: Closer to $1.4 Million

So far we've only added up the bank-related costs: P&I, plus property tax and insurance. That's already ~$1.16 million over 30 years on a $400K home. But owning a home means you also pay for everything inside the walls.

Here's the realistic 30-year ownership outflow, with conservative and high estimates:

| Cost bucket | 30-year total (low) | 30-year total (high) |

|---|---|---|

| Total P&I | $766,428 | $766,428 |

| Property tax (3% annual growth) | $190,000 | $210,000 |

| Insurance (compounding 6-9%) | $200,000 | $340,000 |

| Maintenance (Freddie Mac 1-3%) | $200,000 | $300,000 |

| Major capital replacements | $45,000 | $80,000 |

| True 30-year ownership outflow | ~$1.4M | ~$1.7M |

The capital replacement bucket is the one most people forget. Major systems wear out on predictable schedules:

- Roof: $5,400-$20,000+ for asphalt shingle (typical lifespan 15-30 years). Plan for at least one replacement during ownership.

- HVAC system: $5,000-$15,000 (lifespan 15-25 years). You'll likely replace it twice.

- Water heater: $880-$1,800 (lifespan 8-12 years). Two to three replacements over 30 years.

- Major appliances: $3,000-$8,000 every 10-15 years.

- Exterior paint, deck, fence, driveway: $5,000-$30,000 in cumulative work.

None of this shows up on your mortgage disclosure. None of it shows up on a basic calculator. All of it is real — and it's why the 5-year rule for buying a house often understates the real break-even timeline once maintenance is fully accounted for.

The Escape Hatches (and One Hack That Actually Works)

The math is bleak, but it isn't fixed. There are four levers that materially change the outcome.

1. Biweekly Payments — The Only "Hack" That Works

Pay half your monthly payment every two weeks instead of one full payment monthly. Because there are 26 biweekly periods per year, you make 13 full monthly payments instead of 12 — one extra per year, all going to principal.

This is the genuinely good deal. It costs you nothing extra in cash flow (you still pay the same yearly total), but it shaves over $100K off lifetime interest. You don't need a "biweekly mortgage program" — those are scams that charge $400-$1,000 in setup fees plus monthly service charges. Just send the equivalent extra principal directly to your lender, or ask them to set up biweekly drafts for free.

2. Extra $200 Per Month

Adding $200/month to the regular payment goes 100% to principal:

That extra $200 isn't an expense. At 7%, it's effectively a guaranteed 7% tax-free return — better than most "safe" investments and competitive with stock market historical averages. The same principle is even more powerful on credit card debt, where rates run above 20%: paying anything over the minimum payment is one of the highest-return moves in personal finance.

3. 15-Year vs. 30-Year

If you can afford the higher monthly payment, the 15-year mortgage is dramatically cheaper:

| Term | Rate | Monthly P&I | Total interest | Lifetime savings |

|---|---|---|---|---|

| 30-year fixed | 7.00% | $2,129 | $446,428 | — |

| 15-year fixed | 7.00% | $2,876 | $197,725 | −$248,703 |

The 15-year monthly payment is roughly 35% higher, but you save almost $250K in lifetime interest. In real-world conditions, 15-year rates also typically run 0.5-0.75% lower than 30-year rates, making the savings even bigger.

4. Refinancing if Rates Drop

A single percentage point drop on a $320K loan saves roughly $76,000 in lifetime interest:

| Rate | Monthly P&I | Total interest | Savings vs 7% |

|---|---|---|---|

| 7.00% | $2,129 | $446,428 | — |

| 6.30% (April 2026 avg) | $1,981 | $393,114 | −$53,314 |

| 6.00% | $1,919 | $370,682 | −$75,746 |

| 3.50% (pre-2022) | $1,437 | $197,299 | −$249,129 |

The 3.5% pre-2022 row is the kicker. The same $320K loan that costs $446K in interest at 7% would have cost only $197K at the rates of 2020. Same house. Same loan. Different decade. $249,129 worse just from the rate environment you happened to buy in.

"But Wait — You Forgot About…" (The Counter-Arguments)

The $446K-in-interest framing is brutal but it isn't the whole picture. To be honest, here are the four biggest counter-arguments to "buying is a rip-off":

Inflation erodes the real cost

That $2,129 monthly payment in Year 30 is worth roughly $873 in today's purchasing power at 3% average inflation. Translated to today's dollars, the real (inflation-adjusted) lifetime interest cost is closer to $280,000-$320,000 — still painful, but meaningfully less than the $446K headline.

The mortgage interest deduction (mostly dead post-TCJA)

The Tax Cuts and Jobs Act limited interest deductions to the first $750K of mortgage debt and roughly doubled the standard deduction. For tax year 2026, the standard deduction is $16,100 single / $32,200 married filing jointly. Year 1 interest on a $320K loan at 7% is about $22,300 — alone not enough for a married couple to beat the standard deduction. Only about 10-13% of taxpayers itemize after TCJA. For most middle-class buyers, the mortgage interest deduction is theoretical, not real.

Home appreciation

The FHFA House Price Index data going back to 1991 shows long-term US home appreciation of approximately 4.3% annualized. At that rate, a $400K home becomes worth roughly $1.4M after 30 years (nominally). Subtract inflation and the real appreciation is closer to 1.5%/year. The capital gains exclusion ($250K single / $500K MFJ) means most of that gain is tax-free when you sell.

Forced savings vs. renting

Rent payments build $0 of equity. The $80K down payment plus all that interest does eventually convert into a paid-off house worth ~$1.4M (in nominal dollars). The honest comparison isn't "interest paid vs. zero" — it's "buying outflow vs. rent outflow + investment returns over the same 30 years."

Run that comparison rigorously and the fair verdict is roughly: in most scenarios, owning still wins by $200,000-$400,000 over 30 years vs. renting and investing the difference. But the gap is much smaller than the "$446K interest!" headline suggests. The shocking number is real. The conclusion isn't quite as bleak as the number implies. To run the parallel "what if I invested instead" scenario for yourself, plug your numbers into our investment growth simulator and compare against the home equity outcome.

What Banks Don't Highlight

A few details that don't make it into the "you're approved!" letter:

- Pre-approved doesn't mean affordable. Lenders approve up to 45-50% DTI on conventional loans, 56.9% on FHA. Affordability calculators routinely show "max" numbers that consume 40-50% of your take-home pay. We dug into how much house you can actually afford on a $100K salary — the gap between "lender max" and "sleep at night" is real.

- Escrow shortfalls in year 2. Your initial property tax estimate is based on the previous owner's assessed value. After your purchase resets the assessment, your tax bill jumps and your "fixed" payment increases by $100-$300/month.

- The 50-year mortgage trap. The Trump administration floated a 50-year mortgage proposal in November 2025. On the same $320K loan at 7%, a 50-year version would cut your monthly payment by about $200 — but add roughly $389,000 in extra lifetime interest. The bank wins twice: smaller payment for you, much bigger profit for them.

The One Number That Should Be on Every Mortgage Disclosure

If you remember nothing else from this post, remember the cost-to-loan ratio: total payments divided by amount borrowed.

- 30-year @ 7%: 2.40× ($766K paid on $320K borrowed)

- 30-year @ 6%: 2.16×

- 15-year @ 7%: 1.62×

- 50-year @ 7%: 3.61×

This single ratio tells you, at a glance, how much you're paying back per dollar borrowed. It's the most honest one-number summary of any mortgage. Demand it from your loan officer before signing.

Frequently Asked Questions

How much interest do you actually pay on a $400,000 mortgage?

On a $400K home with 20% down ($80K) leaving a $320,000 loan at 7% over 30 years, you pay $446,428 in interest alone. Total payments: $766,428 — $2.40 returned for every $1 borrowed. Daily cost averages $40.77 for the entire 30 years.

What's the monthly payment on a $400K mortgage?

P&I on a $320,000 loan at 7% / 30-year is $2,128.97. Full PITI with average property tax ($333) and insurance ($208): about $2,670/month — 25% higher than the P&I-only number most basic calculators show.

When does principal exceed interest on a 30-year mortgage?

On a $320K loan at 7%, the principal portion of your monthly payment first exceeds the interest portion at month 242 — early in Year 21. Until then, more than half of every payment is pure interest. The first month is 87.7% interest.

What's the true 30-year cost of owning a $400K home?

P&I ($766K) + property tax (~$200K) + insurance (~$270K) + maintenance (~$250K) + capital replacements (~$60K) = approximately $1.4-$1.7 million total outflow over 30 years.

Do biweekly payments really save money?

Yes. 26 half-payments per year = 13 full monthly payments instead of 12. On a $320K loan at 7%, biweekly saves ~$109,000 in interest and pays off the loan ~6.3 years early. Don't pay a third party for "biweekly programs" — your lender will set this up for free.

How much does an extra $200/month save?

On a $320K loan at 7% over 30 years, $200/month extra principal saves about $119,000 in interest and shortens the loan by 6.8 years. Effectively a 7% guaranteed tax-free return on every extra dollar.

Is a 50-year mortgage a good deal?

No. 50-year at 7% on $320K cuts your payment by ~$200/month but adds ~$389,000 in extra lifetime interest (total goes from $446K to ~$835K). The bank wins twice. Trump's November 2025 50-year proposal drew significant criticism on this exact math.

Why is my mortgage payment so much higher than P&I?

P&I is just principal + interest. Real PITI adds property tax (~$333/mo nationally), insurance (~$208/mo), PMI if under 20% down, and HOA. The gap is typically 25-30%.

Is the mortgage interest deduction still worth it?

For most middle-class buyers, no. Standard deduction for tax year 2026 is $16,100 single / $32,200 MFJ. Year-1 interest on $320K @ 7% is ~$22,300 — alone not enough to beat MFJ standard deduction. Only ~10-13% of taxpayers itemize post-TCJA.

Bottom Line

A $400,000 home at 7% for 30 years really does cost you $446,428 in interest. The PITI really is 25% higher than P&I. The true 30-year ownership cost really is closer to $1.4 million than $400K. None of this means buying is wrong — it means you should buy with your eyes open.

The escape hatches are real too. Biweekly payments save $109K. An extra $200/month saves $119K. A 15-year loan saves $249K. A 1-percentage-point lower rate saves $76K. These aren't marketing pitches — they're math you can verify in 30 seconds.