The 5-Year Rule for Buying a House: When It's Right (and When It's Dead Wrong)

Where the 5-year rule for buying a house came from, why it once worked, and why 2026's mortgage rates and slow appreciation often push real break-even past year 7.

"You should plan to stay at least 5 years before buying makes sense." If you've ever brought up homeownership at a dinner table or in a real estate office, you've heard some version of the 5-year rule for buying a house. It's so common it sounds like settled wisdom — like compound interest, or "don't shop hungry."

So here's the uncomfortable part: the 5-year rule is not a fact. It's a heuristic, and the assumptions underneath it have largely stopped being true. No academic paper defines the 5-year rule. It came from dividing typical sell-side transaction costs (about 8 to 10% of sale price) by the historical home appreciation rate (about 5% per year), which suggested buyers needed roughly 5 years to break even on costs alone. That math worked in the 1990s and early 2000s. It does not describe April 2026.

This guide explains where the 5-year rule comes from, walks through a 2026 worked example using the actual current numbers, and gives you a framework for figuring out your real break-even year — which is almost certainly not 5.

Where the 5-Year Rule for Buying a House Came From

The 5-year rule has no single origin. It crystallized from real estate industry math during a roughly two-decade window when three things happened to be true at once:

- Mortgage rates around 5 to 7%. Affordable enough that most buyers could carry a 30-year fixed without their payment crowding out everything else.

- Home appreciation around 4 to 5% per year. The FHFA House Price Index long-term average since 1991 is 4.4% per year, and 2000s years routinely beat that.

- Stable transaction costs around 6 to 8%. Realtor commissions of 6% combined and closing costs of a few percent on top.

Run those numbers and you get a rough payback of 2 to 3 years on transaction costs alone, plus a margin of safety, and you arrive at the 5-year mantra. Suze Orman still uses 5 years (preferably 10) as her threshold. The NYT Upshot rent vs buy calculator moved the conversation toward computing an actual break-even year per scenario, but the 5-year shorthand stuck around as common wisdom.

The funny thing about today: the average American homeowner now stays much longer than 5 years anyway. The 2025 NAR Profile of Home Buyers and Sellers reports the median seller tenure is now 11 years — a record high. Buyers expect to stay 15 years, and 28% call their purchase a "forever home." ATTOM Q4 2025 data puts the average at 8.55 years, near a 25-year peak. The early-2000s average per NAR was closer to 6 years. Most homeowners today blow past any reasonable break-even simply by staying — but they're staying largely because of the rate lock-in effect: people who locked in 3% mortgages in 2020-2021 do not want to give them up.

How Long Until Buying a House Pays Off in 2026?

The 5-year rule's underlying assumptions have all moved against today's buyer. Run through them one by one:

1. Mortgage rates roughly doubled

The Freddie Mac Primary Mortgage Market Survey reading for the week of April 23, 2026 was 6.23%. The April 16 reading was 6.30%. Either way, that's roughly double the pandemic-era low rates that produced today's median seller tenure. On a $400,000 home with 20% down, the 6.23% monthly principal-and-interest payment is about $1,968. First-year interest alone is around $19,800. Across the first 10 years of that mortgage, the buyer pays about $185,000 in interest before counting any principal as equity.

2. Home appreciation has stalled

Three different national indices tell the same story:

- Case-Shiller national index, January 2026: +0.9% year over year.

- FHFA HPI, January 2026: +1.6% year over year.

- Case-Shiller H2 2025: −1.3%, with all 20 metros negative in the second half.

The 5-year rule was calibrated for ~5% appreciation. Current actual appreciation is about a third of that. Each percentage point of appreciation cuts roughly one year off your break-even. Going from 5% appreciation to 1.5% pushes break-even out by 2 to 4 years just from this single variable.

3. Selling costs did not actually fall after the NAR settlement

The NAR settlement took effect August 17, 2024 and was supposed to reduce broker commissions by separating buyer-side from seller-side compensation. Redfin's tracking shows buyer-agent commissions barely budged — averaging 2.34% in October 2024 versus 2.35% in August 2024. Sellers should still budget 6 to 10% of the sale price in total selling costs (combined commissions plus closing fees plus transfer taxes plus optional concessions). On a $400,000 home that's $24,000 to $40,000 evaporating in friction at the moment of sale.

4. Insurance costs are climbing fast

Insurify projects the average US homeowners insurance premium at $3,057 in 2026, up another 4% after a 12% jump in 2025. California is up 16% year over year. Florida averages near $8,500. None of this was assumed in the original 5-year rule math.

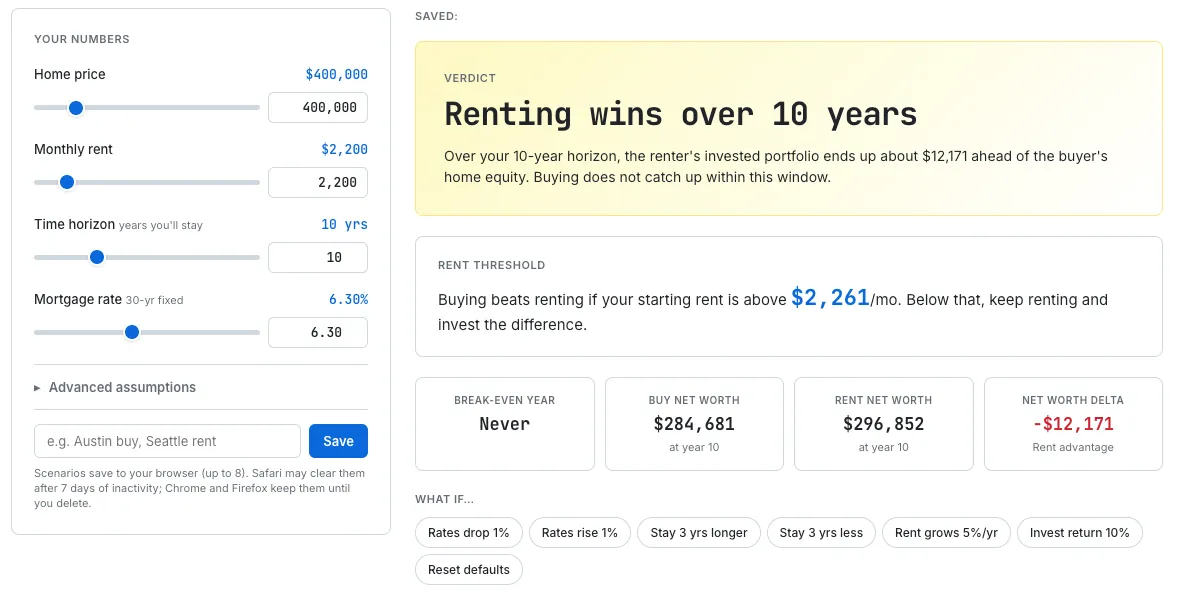

A 2026 Worked Example: $400K Home, $2,200 Rent, 10 Years

Concrete numbers help. Consider a buyer in a mid-sized US metro (think Charlotte, Columbus, or Phoenix) deciding between a $400,000 starter home and a comparable $2,200/month rental.

Inputs:

- Home price $400,000; down payment 20% ($80,000); mortgage 6.23%, 30-year fixed

- Property tax 1.0% of value; insurance 1.0%; maintenance 1.0%; HOA $0

- Buy closing 3% ($12,000); sell closing 7% (on appreciated price)

- Comparable rent $2,200/month, growing 3%/year

- Investment return on the renter's portfolio: 7% nominal (the conservative planner default — historical S&P 500 long-run total return is roughly 10%, so 7% is on the cautious side)

- Two appreciation scenarios: 4% (long-run norm) vs 1.5% (today's actual)

Running this through the Rent vs Buy Calculator, the results split sharply by appreciation scenario:

The default scenario at April 2026 rates: with 6.23% mortgages and the inputs above, renting comes out ahead at year 10 in the conservative case. Run your own numbers in the Rent vs Buy Calculator.

Scenario A — 4% long-run appreciation:

- Year 5: buyer is roughly $28,000 behind the renter (the 5-year rule has already failed by tens of thousands)

- Year 7-8: rough break-even

- Year 10: buyer is approximately $58,000 ahead

Scenario B — 1.5% appreciation (today's actual):

- Year 5: buyer is roughly $52,000 behind

- Year 10: buyer is still about $31,000 behind

- Break-even: does not occur within a 10-year horizon

The 5-year rule does not just fail by a year or two in this environment. It can fail by enough that selling at year 5 would burn $50,000 of your savings versus renting and investing the down payment.

The Four Variables That Actually Determine Your Break-Even

Forget the number 5. Your real break-even depends on four variables. Move any one of them and the answer shifts dramatically.

Variable 1: The spread between your mortgage rate and your investment return

This is the single biggest lever. If you're paying 6.23% on the mortgage and your alternative is a portfolio earning 7% nominal, the spread is essentially zero. Money locked in your home equity is earning the same rate as money in the index fund — and you've also paid a fortune in transaction costs to put it there.

Compare 2021's environment: 3% mortgage rate vs 7% expected stock returns is a 4-point spread that strongly favors borrowing cheap and putting equity to work. That's why the 5-year rule still felt true in 2021. The spread, not the calendar, drives break-even.

Variable 2: Home appreciation rate

Each percentage point of annual appreciation moves break-even by roughly one year. The FHFA's long-run national average is 4.4% per year since 1991, but as we showed above, current actual appreciation is closer to 1 to 2%. If your local market is appreciating below 2%, plan on break-even being significantly later than the national average. Look up your specific metro in FHFA's HPI data.

Variable 3: Starting rent and rent growth

The higher your local rent, the faster owning catches up. BLS CPI Rent of Primary Residence ran +3.4% year over year in Boston as of March 2026. Each percentage point of rent growth shaves time off break-even. If a comparable rental is 80% or more of your full PITI payment, owning starts winning quickly. If it's 60% or less, renting can stay ahead for a long time.

Variable 4: Total transaction costs

Buy closing 2-5%, sell closing 6-10%. Combined that's 10-13% of home value lost to friction. This single variable wipes out roughly a decade of typical appreciation and is the main reason short-tenure buying is rarely a financial win. The NAR settlement was supposed to compress these but, per Redfin's data above, change has been minimal.

What Top Personal Finance Voices Actually Say

Three of the most-cited voices in personal finance have publicly disagreed with a one-size-fits-all 5-year rule for years.

Ramit Sethi (I Will Teach You To Be Rich) frames it bluntly: rent is the maximum you'll pay each month — your landlord absorbs surprise repairs, taxes, and insurance shocks. A mortgage is the minimum you'll pay; everything from new HVAC to property tax reassessment to insurance hikes lands on you. Sethi's "phantom costs" estimate is that ownership adds 30 to 50% on top of the bare mortgage payment.

Ben Felix (PWL Capital) coined the 5% rule: a home's annual unrecoverable cost is roughly 1% property tax + 1% maintenance + 3% opportunity cost on the down payment, totaling 5% of home value per year. If a comparable rental costs less than 5% of the home's price annually, renting is mathematically better. On a $400,000 home that threshold is $20,000/year or $1,667/month. His 2024 Canadian study found that renters who invested the cost difference outperformed buyers in 7 of 12 cities over 20 years (2005-2024).

Dave Ramsey is generally pro-buying long-term but enforces strict conditions: debt-free, full emergency fund, 10-20% down, payment ≤25% of take-home pay, ideally a 15-year fixed. If any condition isn't met, he tells you to keep renting.

The 2026 consensus across these voices isn't "5 years": it's "calculate your specific break-even and add a buffer."

Does the 5-Year Rule Apply to Your Situation? A Decision Checklist

Run through these five questions. If you can't say "yes" to at least four of them, treat the 5-year rule as wrong for you and either rent longer or expect to stay much longer than 5 years before buying.

- Does the calculator show your specific break-even at 7 years or fewer? Run your numbers in the Rent vs Buy Calculator with your actual home price, rent, and rate.

- Is your mortgage rate at least 2 percentage points below your expected investment return? If yes, the spread favors owning. If your mortgage is 6.23% and your expected return is 7%, the spread is 0.77 — borderline.

- Is your local price-to-rent ratio under 16? Above 21 strongly favors renting. SF, Seattle, and other expensive coastal metros sit in the 30s.

- Is local annual appreciation tracking above 3%? Below 2% means the math turns adversarial.

- Is your job and family situation stable for 7 years or more? If you might need to relocate or downsize within that window, the friction costs of selling early will likely exceed any equity built.

The 5-year rule is a relic of a specific market. For most buyers in 2026, the honest answer is closer to 7 to 10 years before buying clearly wins — and in slow-appreciation markets, sometimes much longer. The good news: the median American homeowner already plans to stay 15 years. If you're one of them, the timing question matters less than running the actual numbers for your situation.