Is Renting Throwing Money Away? The Math Says No (Sometimes)

The slogan is almost 80 years old. The math behind it stopped working decades ago. Here's where the idea came from and what the numbers actually say in 2026.

"Why are you still renting? You're just throwing money away." If you've heard this once, you've heard it a hundred times — at family dinners, in real estate offices, in the algorithm-driven advice on every social platform. Is renting throwing money away? The honest answer is: no, not as a blanket rule, and the slogan itself is a marketing artifact from a very specific moment in American housing history.

This guide does two things. First, it traces where the "renting is wasted money" idea actually came from — it's not 200 years of accumulated wisdom; it's a roughly 80-year-old narrative built by federal policy and a single suburban developer. Second, it walks through the 2026 math that explains why the slogan fails most modern renters: opportunity cost on the down payment, the 10 to 13% transaction friction of buying and selling, and the often-ignored "phantom costs" of ownership.

Where "Renting Is Throwing Money Away" Actually Came From

The phrase has no single inventor. It crystallized in the late 1940s out of three forces that, together, were designed to convert working-class Americans from renters into homeowners.

Federal policy. The GI Bill of 1944 and the FHA's expansion in the late 1940s redirected billions of federally backstopped dollars toward 30-year, low-down-payment mortgages aimed specifically at working-class buyers. The Housing Act of 1949 codified the goal of "a decent home and a suitable living environment for every American family" — but the mechanism was tilted heavily toward homeownership rather than rental support.

Mass-builder marketing. William Levitt's Levittown opened on Long Island in 1947 with houses priced around $7,000. The mortgage payment was about $58 per month — comparable to or below typical New York rent of the era, making the slogan "rent is wasted money" feel mathematically obvious for that specific cohort. GE, Whirlpool, and FHA-adjacent ad campaigns in the 1950s sold the suburban single-family home as the moral fulfillment of the American Dream.

Cultural framing. The US homeownership rate rose from 44% in 1940 to 62% in 1960. The slogan became conventional wisdom — repeated by realtors, bank ads, and parents — and survived long after the conditions that made it true had vanished. It's worth noting the original 1940s narrative was also racially exclusionary by design: Levittown's deeds explicitly barred Black buyers, embedding the homeownership message in a system that defined who was eligible for it.

The point isn't to relitigate 1940s housing policy. It's to recognize that "renting is throwing money away" was never a neutral observation; it was a manufactured narrative built when fixed credit was cheap, rentals were scarce, and home prices were poised to grow with the postwar economy. The economic conditions of 1948 do not exist in 2026.

Buyers Are Renting Too — From the Bank, the Government, and Time

The most underappreciated fact about ownership: most of a buyer's monthly payment in the early years is not building equity. It's rent in everything but name.

Take a $400,000 home, 20% down ($80,000), 6.23% 30-year fixed (the Freddie Mac PMMS rate for the week of April 23, 2026):

- Monthly principal-and-interest payment: about $1,968

- Year-1 interest paid: roughly $19,800

- Year-1 principal paid: only about $3,820

- Cumulative interest in the first 10 years: roughly $185,000

That's $185,000 paid to the bank to "rent" $320,000 of capital over a decade. Add the rest:

- Property tax (rent on land from the government): about 1% of value nationally — $4,000/year

- Homeowners insurance (rent on risk): national average $3,057 in 2026, after a 12% jump in 2025

- Maintenance (rent on the home's depreciation): typically estimated at 1-1.5% of value annually — $4,000-$6,000/year

- PMI if down payment is below 20%: 0.46-1.5% of loan balance per year

In year one, a buyer pays roughly $30,000-$32,000 in non-equity-building costs before a single dollar of principal counts as equity.

Ramit Sethi has a useful frame for this: "Rent is the maximum you'll pay each month. A mortgage is the minimum." The renter knows their cost. The owner finds out as repairs, tax reassessments, and insurance hikes accumulate. He estimates these "phantom costs" add 30 to 50% on top of the bare mortgage payment.

The Opportunity Cost of a Locked-Up Down Payment

The second number the slogan ignores: your down payment could have been doing something else.

The historical S&P 500 has produced about a 10% long-run nominal total return (Damodaran NYU dataset, 1928-present). Conservative financial planners typically use 7% to account for fees and execution drag. At a 7% annual return:

| Time horizon | $80,000 at 7% nominal | $80,000 at 10% nominal |

|---|---|---|

| 10 years | ~$157,000 | ~$208,000 |

| 20 years | ~$310,000 | ~$538,000 |

| 30 years | ~$609,000 | ~$1,400,000 |

Compare those numbers to what a home does to the same money. Robert Shiller's data shows US home real returns were roughly flat from 1890 to 1997, only rising to about 6% annually since 1998. Home equity is structurally a slower-compounding asset than diversified equities.

The catch — and this is the honest version — most renters do not actually invest the difference. The 2022 Federal Reserve Survey of Consumer Finances shows median renter financial wealth around $960 versus dramatically higher figures for owners. The Cleveland Fed's 2021 analysis argues most of this gap reflects selection effects and forced savings rather than homeownership being a uniquely powerful investment. The math favors renting only when the renter has the discipline to actually invest the saved cash.

The 10–13% Friction You Pay Just to Buy and Sell

The third hidden cost: buying a home and later selling it costs roughly 10 to 13% of the home's value in transaction friction. Buy-side closing costs typically run 2 to 5% of price (loan origination, title insurance, appraisal, inspections). Sell-side closing costs total another 6 to 10% (commissions, transfer taxes, title, attorney, concessions).

The August 2024 NAR settlement was supposed to compress this. Redfin's tracking shows buyer-agent commissions barely budged: 2.34% in October 2024 vs 2.35% in August 2024. Combined commissions plus other selling costs still total 6 to 10%.

On a $400,000 home, that's $40,000 to $52,000 evaporating in friction across the round-trip. To break even, your home needs to appreciate enough to overcome that friction before any equity accrues to you. With Case-Shiller appreciation at 0.9% year over year, that's roughly 5 to 7 years of appreciation just to cover the cost of the round-trip.

What Personal Finance Experts Actually Say

Ramit Sethi: "Never, ever say you're throwing money away on rent." He has personally rented in NYC, SF, and LA by choice and argues phantom costs add 30-50% on top of the mortgage payment. Renting buys flexibility, predictability, and freedom from major repair surprises.

Ben Felix (PWL Capital): The 5% rule says a home's annual unrecoverable cost is roughly 1% property tax + 1% maintenance + 3% opportunity cost = 5% of the home's value per year. If a comparable rental costs less than 5% of price annually, renting is mathematically better. His 2024 Canadian study found renters who invested the cost difference outperformed buyers in 7 of 12 cities over 2005-2024.

Morgan Housel: "Renting until our early 30s was probably the best financial decision my wife and I ever made." He bought later for stability and lifestyle, not investment returns. He has written that homeownership's financial rewards are "overstated."

Cleveland Fed (2021): The wealth gap between owners and renters is "quite challenging" to attribute causally to homeownership; selection effects (savers self-select into ownership) are large.

Counterpoint — Dave Ramsey: Pro-buying long-term, but his conditions are strict: debt-free, full emergency fund, 10-20% down, payment ≤25% of take-home, ideally a 15-year fixed. "Renting is not a waste of money. It's buying patience."

The Wealth Gap Between Owners and Renters (and What It Really Shows)

The most-cited counterpoint to "renting is fine" is the wealth gap. The 2022 Federal Reserve Survey of Consumer Finances found median net worth for homeowners was $396,200 — roughly 38 times the $10,400 median for renters.

That gap looks devastating. But the Cleveland Fed and the Joint Center for Housing Studies at Harvard have both argued the gap is largely explained by selection effects plus forced savings, not by homeownership being uniquely lucrative. People who can save 20% down already have higher savings propensities and more stable incomes. The mortgage payment then forces them to keep saving every month. Strip out those two effects and the homeownership "premium" shrinks dramatically.

In other words: homeowners didn't get rich because they bought. People who were going to get rich bought. The math is correlation, not pure causation.

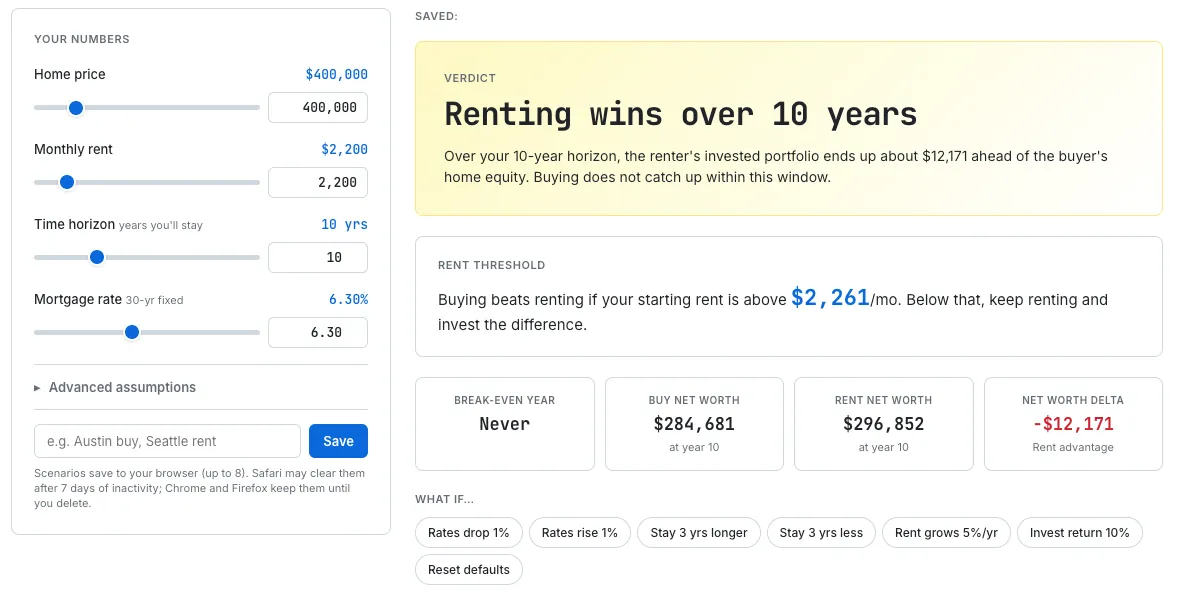

A 2026 Comparison: $400K Home vs $2,200 Rent

Concrete numbers for the same buyer profile from the previous section. Inputs: $400,000 home, 20% down, 6.23% mortgage; comparable rent $2,200/month at 3% growth; investment return 7% nominal; 4% home appreciation; 1% property tax, 1% insurance, 1% maintenance; sell at year 10 at 7% closing costs.

The default scenario in the Rent vs Buy Calculator at April 2026 rates: at 6.23% mortgage and 4% appreciation, renting plus investing the down payment edges out buying within a 10-year horizon. The numbers below break down why.

| Metric (10 years) | Buyer | Renter (invests difference) |

|---|---|---|

| Year-1 monthly outlay | ~$2,810 (PITI + maintenance) | ~$2,220 (rent + insurance) |

| Cumulative non-equity outlay (10 yrs) | ~$300,000 | ~$305,000 |

| Home equity (after 8% sell costs) | ~$225,000 | $0 |

| Investment portfolio | $0 (down payment in walls) | ~$242,000 |

| Net financial position year 10 | ~$225,000 | ~$242,000 |

The renter ends up about $17,000 ahead after 10 years — but only if they actually invest the cost difference. Bump appreciation to 6% (a strong market) and the buyer pulls ahead. Drop investment return to 5% (cautious) and the buyer pulls ahead. The answer depends entirely on which assumptions you make. That's why the slogan fails: there is no universal answer.

It's worth comparing this to Bankrate's April 2025 finding that renting is now cheaper on a monthly basis than buying in all 50 of the largest US metros, with mortgage payments averaging 38% above rent. In other words: in current 2026 conditions, the cash-flow side strongly favors renting in nearly every American city.

Four Cases Where Renting Wins, Four Where Buying Wins

To be honest with the math, here's the symmetric version.

Renting wins when…

- Local price-to-rent ratio is high. Above 18 favors renting; above 25 strongly favors renting. San Francisco and Seattle are around 36; Manhattan even higher.

- You might move within 5 years. Transaction friction of 10-13% rarely amortizes that fast.

- You have the discipline to invest the cost difference. Ben Felix's renter wins were entirely conditional on this. Without it, owning is the better forced-savings vehicle.

- You're buying late-cycle or in a volatile market. Shiller's data on the early 2000s reminds us leverage cuts both ways.

Buying wins when…

- You'll stay 10+ years. Amortization compounds, transaction costs amortize, and forced-savings effects accumulate.

- Your local rent is rising fast. A fixed mortgage payment becomes a hedge against the 3-5% annual rent inflation US renters have faced since 2022.

- You need forced savings. Most people, in practice, don't actually invest the difference. The mortgage payment behaves as an automatic savings plan.

- Stability and lifestyle have real value to you. Roots, kids in school, the freedom to renovate. Spreadsheets don't capture this, but it's not zero.

The Honest Answer

"Renting is throwing money away" was a marketing slogan from 1948. It described a specific moment when fixed credit was newly cheap, rentals were scarce, and federal policy was actively pushing the working class into ownership. None of those conditions describe 2026.

The math today is more honest: renting is not waste; it's a different financial path with different trade-offs. Buyers also "rent" — from the bank in interest, from the government in taxes, from insurance companies, from time itself in maintenance. The right question isn't "should I throw money away on rent?" — it's "do my numbers, my city, my horizon, and my discipline favor one path over the other?"

That's a question you can actually answer.