Compound Interest Explained: How Your Money Grows Over Time

From a 4,400-year-old Babylonian clay tablet to Benjamin Franklin's 200-year experiment — how compound interest works, why starting early matters, and what most calculators get wrong about fees, taxes, and inflation.

In 1790, Benjamin Franklin left a special provision in his will. He donated approximately $4,400 each to the cities of Boston and Philadelphia — with the condition that the money be invested at compound interest for 200 years. By 1990, those gifts had grown to a combined $6.5 million — roughly $4.5 million in Boston and $2 million in Philadelphia (Philanthropy Roundtable). Franklin's experiment remains the most dramatic real-world demonstration of the power of compound interest.

"Compound interest is the eighth wonder of the world" is widely attributed to Albert Einstein — but Einstein never said it. According to Quote Investigator and Snopes, the quote was first attributed to Einstein in a 1976 Wall Street Journal column — 21 years after his death. But regardless of who said it, the power of compound interest is very real.

This guide explains what compound interest is, how it works, why starting early matters so much, and how fees, taxes, and inflation quietly erode your investment returns. Whether you're just starting to invest or planning for retirement, you'll walk away with a clear understanding of the most powerful force in personal finance.

What Is Compound Interest?

Compound interest is interest calculated on both the original principal and all previously accumulated interest. In simple terms, it's "interest on interest" (SEC, Investor.gov).

Simple Interest vs. Compound Interest

Simple interest is calculated only on the original principal. If you invest $10,000 at 5% simple interest for 10 years, you earn $500 per year — $5,000 total — for a final balance of $15,000.

Compound interest accelerates growth because each year's interest earns interest the following year. The same $10,000 at 5% compounded annually for 10 years grows to $16,289 — $1,289 more than simple interest. The longer the time period, the wider this gap becomes.

The Rule of 72

The Rule of 72 is a quick way to estimate how long it takes for your money to double: divide 72 by the annual rate of return.

- At 6%: 72 ÷ 6 = 12 years to double

- At 9%: 72 ÷ 9 = 8 years to double

- At 12%: 72 ÷ 12 = 6 years to double

The rule is most accurate in the 6–10% range. The exact mathematical constant is 69.3 (for continuous compounding), but 72 is used because it divides evenly by more common rates.

How Compounding Frequency Matters

How often interest is compounded — daily, monthly, or annually — also affects the result. Here's $10,000 at 5% for 10 years:

| Compounding Frequency | Balance After 10 Years | Difference |

|---|---|---|

| Annual | $16,289 | Baseline |

| Monthly | $16,470 | +$181 |

| Daily | $16,487 | +$198 |

The jump from annual to monthly compounding is far more significant than from monthly to daily. The key takeaway: the rate of return and time invested matter far more than compounding frequency.

A Real Example: $10,000 at 7% for 30 Years

$10,000 invested at 7% annual compound interest for 30 years grows to approximately $76,123 (Investor.gov calculator). That's 7.6x the original investment, with $66,123 coming purely from compound interest. At 6% the result would be $57,435; at 10%, $174,494. A few percentage points in return make a difference of tens of thousands of dollars.

A Brief History of Compound Interest

Compound interest is not a modern invention. Its history stretches back to the very beginnings of civilization.

Babylonian Clay Tablets (~2000–1700 BC)

The concept of interest originated in Sumer around 2600–2350 BC — the Sumerian words "mas" (interest) and "ur5-(ra)" (interest-bearing loan) date to this period. The oldest surviving compound interest calculation appears on a Babylonian clay tablet from roughly 2000–1700 BC. It poses the problem: "How long does it take a loan to double at 20% annual compound interest?" The answer recorded on the tablet: approximately 3 years and 283 days, calculated using linear interpolation on a 360-day Babylonian calendar (Cambridge University Press).

Benjamin Franklin's 200-Year Experiment

Franklin was inspired by a French satirical novel featuring a character who collected compound interest for 500 years. He decided to try it in real life. In his 1790 will, he donated 1,000 pounds sterling (about $4,400) to each of Boston and Philadelphia — with the condition that the funds be invested at compound interest for 200 years.

After 100 years (1890), Boston's fund had grown to $391,000. Philadelphia's reached only $172,350 — same starting amount, same time period, but different management produced vastly different results. After 200 years (1990), the combined total was approximately $6.5 million. The experiment proved the power of compound interest while also showing that real-world returns depend heavily on management and conditions (The Franklin Institute).

"Einstein's Eighth Wonder" — Fact Check

"Compound interest is the eighth wonder of the world" is widely attributed to Albert Einstein. This is not true. According to Quote Investigator, a similar phrase first appeared in a 1925 advertisement for the Equity Savings & Loan Company in Cleveland, with no attribution. The first documented attribution to Einstein was in a 1976 Wall Street Journal column — 21 years after his death in 1955. The quote has also been attributed to Baron Rothschild and John D. Rockefeller, with no verified source in any case (Snopes).

Why Starting Early Matters So Much

The most important variable in compound interest is not the rate of return. It's time.

Age 25 vs. 35: What 10 Years Costs You

Assume you invest $200 per month at a 7% annual return:

| Starting Age | Years Invested | Total Contributions | Estimated Balance at 65 |

|---|---|---|---|

| 25 | 40 years | $96,000 | ~$525,000 |

| 35 | 30 years | $72,000 | ~$244,000 |

| 45 | 20 years | $48,000 | ~$106,000 |

The person who starts at 25 contributes only $24,000 more (33%) than the person who starts at 35, yet ends up with $281,000 more. The lost wealth isn't from missed contributions — it's from the 10 years of compounding time that can never be recovered.

Warren Buffett's Timeline

Warren Buffett is one of the most successful investors in history, but his secret isn't just investing skill — it's time.

- Age 30: first $1 million

- Age 56: became a billionaire

- 99% of his wealth was accumulated after age 50

- ~95% was accumulated after age 65

Buffett himself has said: "The biggest thing about making money is time. You don't have to be particularly smart, you just have to be patient." As Morgan Housel wrote in The Psychology of Money (2020): "Buffett's skill is investing, but his secret is time."

The Cost of Every Single Year

This isn't abstract. A $1,000 lump sum invested at 7% at age 25 grows to $14,974 by age 65 (40 years). The same $1,000 invested at age 35 grows to only $7,612 (30 years) — less than half.

The Enemies of Compound Interest — Fees, Taxes, and Inflation

Most compound interest calculators show a beautiful growth curve. In reality, three forces quietly eat away at that curve.

Fees — Compound Interest in Reverse

Investment fees (expense ratios) also compound — but against you. Fees reduce your returns, and the returns those fees would have generated are also lost to compounding.

The same reversal shows up with debt. Carry a balance on a credit card and compounding works relentlessly against you instead of for you — which is exactly why the order you pay cards off in, debt snowball vs avalanche, changes how much interest you ultimately hand the bank.

$100,000 invested for 30 years at 10% annual return:

- 0.03% fee (low-cost index fund): final balance ~$1,720,000

- 1.00% fee (average active fund): final balance ~$1,320,000

- Difference: over $400,000 — more than 4x the original investment lost to fees

Vanguard's research found that expense ratio is the most dominant variable explaining an index fund's excess return. As of 2024, average expense ratios are 0.40% for equity mutual funds and 0.14% for equity ETFs.

Taxes — The Annual Drain

According to Morningstar research, the average US equity mutual fund loses approximately 1.5% of pre-tax returns annually to taxes. Passive S&P 500 index funds have much lower tax drag — only 0.3–0.4% annualized. Over 30 years, this difference compounds into tens of thousands of dollars.

Inflation — The Silent Purchasing Power Thief

The long-term average US inflation rate is approximately 3.2% per year (BLS, since 1913; precisely 3.16%). Applying the Rule of 72, prices double roughly every 23 years. Today's $1,000,000 will be worth only about $400,000 in purchasing power 30 years from now.

The S&P 500's historical average return is ~10% nominal, but after inflation the real return is approximately ~7% (NYU Stern, Damodaran). Always plan your investments using real (inflation-adjusted) returns.

FIRE and the 4% Rule

There's a movement that takes compound interest to its logical extreme — FIRE (Financial Independence, Retire Early).

What Is FIRE?

FIRE is a personal finance movement where people save 50–70% of their income and invest aggressively, aiming to accumulate enough assets to cover living expenses without traditional employment — often decades before the conventional retirement age. It originated with Vicki Robin's Your Money or Your Life (1992) and was popularized among millennials by the Mr. Money Mustache blog (2011).

The 4% Rule and the Trinity Study

In 1994, financial advisor William Bengen analyzed market data going back to 1926 and found that retirees with a 50/50 stock-bond portfolio could safely withdraw 4% per year (adjusted for inflation) and sustain their portfolio for at least 30 years. In 1998, the Trinity Study by Cooley, Hubbard, and Walz at Trinity University confirmed this finding.

Flipping it gives the 25x Rule: save 25 times your annual expenses and you can retire. Need $40,000 per year? Save $1,000,000. Need $60,000? Save $1,500,000.

Morningstar's 2025 edition of "The State of Retirement Income" puts the safe withdrawal rate for 2026 retirees at 3.9% (assuming a 90% probability of funds lasting 30 years).

Types of FIRE

- Lean FIRE — Minimal living expenses, smaller portfolio required

- Fat FIRE — Maintaining or exceeding a middle-class lifestyle

- Coast FIRE — Save aggressively early, then let compounding do the rest without additional contributions

- Barista FIRE — Semi-retirement with part-time work for supplemental income and benefits

Limitations and Criticisms

The 4% rule was designed for a 30-year retirement. Someone retiring at 35 may need funds for 50–65 years. Sequence-of-returns risk — a market crash in the early years of retirement — can devastate a portfolio. Healthcare costs before Medicare eligibility (roughly $380,000 in the US), unpredictable expenses, and the reality that saving 50–70% of income is unrealistic for most people are key criticisms.

Common Investment Mistakes to Avoid

The magic of compound interest only works if you maintain the right behavior over a long period. But many investors sabotage themselves.

Trying to Time the Market

Over 30 years (1995–2025), missing the S&P 500's best 10 days cut total returns roughly in half. Missing the best 30 days reduced annual returns from 8.4% to 2.1%. Missing the best 50 days turned returns negative. The critical insight: 7 of the 10 best days occurred within two weeks of the market's largest declines (Hartford Funds).

Emotional Selling

The DALBAR 2024 study found that the S&P 500 returned 25.02%, but the average equity investor earned only 16.54% — an 8.48 percentage point gap. On $100,000, that's over $12,000 lost in a single year from poor timing. DALBAR's "Guess Right Ratio" hit a record low of 25% — investors correctly timed their moves only one quarter of the time.

Ignoring Fees

$100,000 invested at 7% for 30 years: a 0.5% fee (net 6.5%) yields approximately $661,000; a 1.5% fee (net 5.5%) yields approximately $498,000 — a difference of roughly $163,000. A 1% difference in fees can erase 25% of your final retirement balance.

Starting Too Late

Investing $200/month at 7%: starting at age 25 yields approximately $525,000 by 65; starting at 35 yields approximately $244,000. The 10-year difference costs about $281,000 — 23 times the additional $12,000 in contributions.

Calculate Compound Interest for Yourself

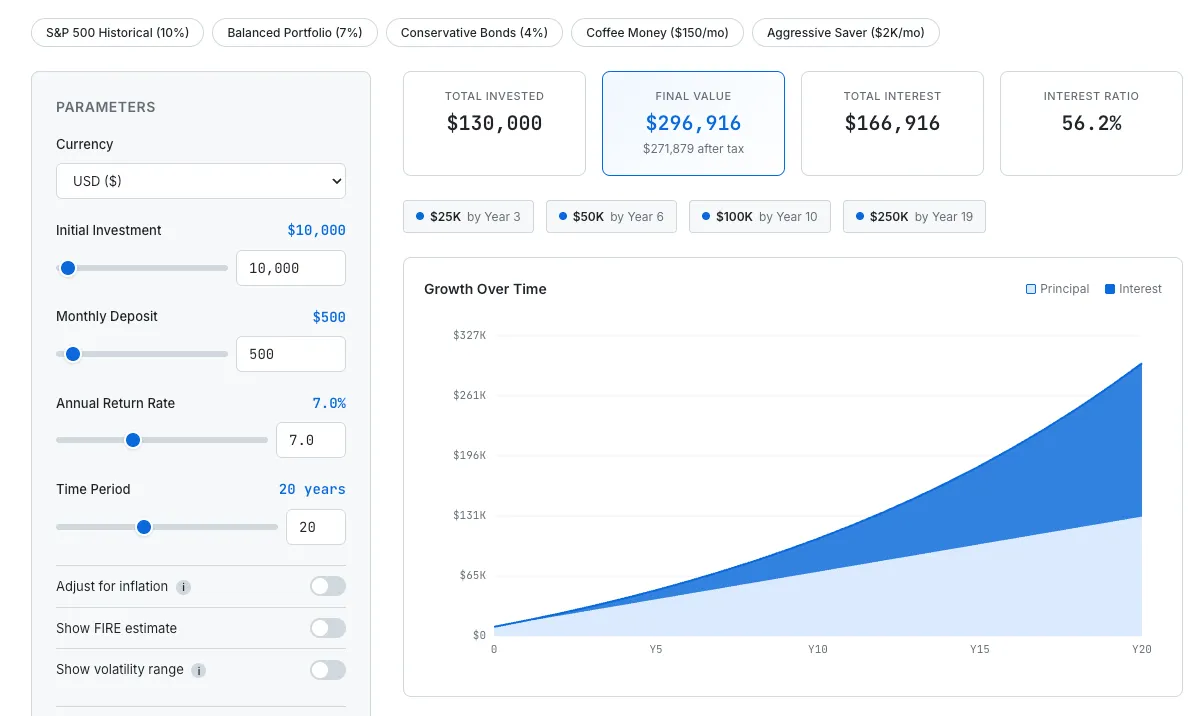

Once you understand how compound interest works, the most important next step is to run the numbers with your own figures. Enter your initial investment, monthly contributions, and expected return to see how your money grows over 10, 20, or 30 years — and critically, to see how fees, taxes, and inflation erode that growth. Those monthly contributions come out of what you earn, and seeing what your salary is really worth per second makes the trade-off between spending today and investing for later far more concrete.

SudoTool's Investment Growth Simulator includes what most compound interest calculators leave out. Enter an expense ratio and capital gains tax rate to see after-tax returns. Toggle inflation adjustment to convert future balances into today's purchasing power. The FIRE estimate (4% Rule) shows how much monthly, annual, and daily income your portfolio could generate — turning an abstract number into a concrete "can I retire on this?" answer. A Monte Carlo Lite volatility band shows optimistic and pessimistic scenarios instead of a single unrealistic smooth line. All calculations run in your browser — no data is sent to any server.

SudoTool Investment Growth Simulator — calculate compound interest with fees, taxes, inflation, and FIRE income estimates.

Frequently Asked Questions

What is compound interest?

Compound interest is interest calculated on both the original principal and all previously accumulated interest — "interest on interest." Unlike simple interest, it causes growth to accelerate over time. In long-term investing, the majority of returns come from the compounding effect.

What is the Rule of 72?

Divide 72 by the annual interest rate to estimate how many years it takes for your money to double. At 8% annual return: 72 ÷ 8 = approximately 9 years to double. It's most accurate in the 6–10% range.

Did Einstein really call compound interest the "eighth wonder of the world"?

No. According to Quote Investigator and Snopes, the earliest known attribution to Einstein was in a 1976 Wall Street Journal column — 21 years after his death. No verified source exists. The quote has also been attributed to Baron Rothschild and Rockefeller with no evidence.

Does a 1% difference in fees really matter?

Enormously. $100,000 invested at 10% for 30 years: the difference between a 0.03% fee and a 1% fee is over $400,000 in final value. Fees compound against you — a small difference magnifies dramatically over decades.

What is the historical average return of the S&P 500?

Since 1928, the S&P 500 has averaged approximately 10% nominal annual return. Adjusted for inflation, the real return is approximately 6.5–7.3%. Always plan investments using inflation-adjusted (real) returns.

What is the 4% Rule?

A guideline stating that retirees can withdraw 4% of their portfolio annually (adjusted for inflation) and sustain their funds for at least 30 years. Published by William Bengen in 1994 and confirmed by the Trinity Study in 1998. The inverse — the 25x Rule — says saving 25 times your annual expenses is enough to retire.

Why shouldn't I try to time the market?

Missing the best 10 days in 30 years cuts your returns roughly in half. Missing 50 days turns returns negative. Most of the best days occur within two weeks of the worst days — so investors who sell in panic miss the biggest rebounds.

Is it ever too late to start investing?

The best time to start was yesterday. The second best time is today. Starting earlier gives compound interest more time to work, but starting at any age is always better than not starting at all. The key is to begin as soon as possible, invest consistently, keep fees low, and stay invested for the long term.

Compound Interest — Your Most Powerful Tool

Three things to remember about compound interest:

Time is the most important factor — start as early as you can. 99% of Warren Buffett's wealth was built after age 50. Fees, taxes, and inflation are compound interest's enemies — a 1% fee difference can cost over $400,000 over 30 years. Consider low-cost index funds. Don't try to beat the market — missing just 10 of the best days in 30 years cuts your returns in half. Stay invested.

If you want to calculate compound interest with your own numbers — including fees, taxes, inflation, and FIRE estimates — try SudoTool's Investment Growth Simulator.

Curious about how this tool was built? Read how we built a browser-based investment simulator — the design decisions, technical trade-offs, and lessons learned along the way.