Debt Snowball vs Avalanche: Which Actually Pays Off Credit Cards Faster?

One method is mathematically optimal. The other is what actually gets people to zero. A 2023 peer-reviewed paper puts a $46 billion price tag on the difference — and shows who pays it.

The debt snowball vs avalanche debate is the most-repeated question in consumer finance, and it almost always gets answered badly. Dave Ramsey has taught the snowball method — paying off the smallest balance first, regardless of interest rate — to roughly 10 million Americans through Financial Peace University. One strategy, one rule, millions of followers.

Meanwhile, a 2023 paper in the Southern Economic Journal says this:

— Hamilton (2023), Southern Economic Journal 89(3): 830-859

Translation: Americans pay their banks $46 to $54 billion extra every year because they use snowball instead of the mathematically optimal strategy — the debt avalanche, where you attack the highest-APR card first.

So is the answer simple? Avalanche wins? Not quite. This is the honest comparison that the other 90% of articles on this topic skip. With the average US credit card APR sitting at 21.52% as of February 2026 (Fed G.19) and total US credit card debt at a record $1.28 trillion (NY Fed Q4 2025), the method you pick can mean a difference of $150 to several thousand dollars. But the bigger question is: which method will you actually finish?

Debt Snowball vs Avalanche: The Two Methods in 60 Seconds Each

Both methods start the same way — pay the minimum on every card, every month. The only difference is where the extra money goes.

The Debt Snowball Rule

Throw every extra dollar at the card with the smallest balance. Ignore interest rates. When that card is paid off, its freed minimum payment rolls into the next-smallest card — that's the "snowball" effect.

Suppose you have three cards:

| Card | Balance | APR |

|---|---|---|

| Store Card | $1,500 | 29% |

| Main Card | $4,000 | 22% |

| Balance Transfer Card | $6,000 | 18% |

Snowball order: Store Card → Main Card → Balance Transfer Card (ascending by balance).

Why this strategy resonates with so many: Ramsey himself put it this way on X in 2019:

And the Ramsey Solutions snowball-vs-avalanche page puts the case bluntly:

In one line: snowball trades some interest cost for faster emotional wins and a higher probability you actually finish.

The Debt Avalanche Rule

Throw every extra dollar at the card with the highest APR. Ignore balances.

Using the same three cards, avalanche order is Store Card (29%) → Main Card (22%) → Balance Transfer Card (18%). In this specific case the order happens to match snowball's — because the smallest-balance card is also the highest-APR card. When that happens, the two methods produce identical results.

Real card portfolios usually diverge. A common case: a $1,000 store card at 18% and an $8,000 main card at 22%.

- Snowball: store card ($1,000) first, then main card.

- Avalanche: main card (22%) first, then store card.

Why avalanche is mathematically optimal: every month, interest accrues on the unpaid balance. A dollar on a 22% card produces $0.0183 of interest per month; a dollar on an 18% card produces $0.015. Killing the card that's generating interest fastest minimizes total interest paid. That's the math Hamilton (2023) quantified at the national level.

What the Research Actually Says (Where Ramsey Is Half-Right)

Here's the part most search results skip.

Gal & McShane (2012) — the original snowball study

David Gal and Blakeley McShane of Northwestern's Kellogg School of Management analyzed about 6,000 clients of a US debt settlement program. Their paper, published in the Journal of Marketing Research 49(4): 487-501, found:

— David Gal, Kellogg Northwestern press release

Translation: the number of accounts closed predicted success better than the dollar amount paid down. Small victories create momentum. Gal himself added the caveat: "From a rational perspective, you should always pay the higher interest balances first." The Kellogg finding doesn't endorse snowball as optimal — it explains why snowball works in practice even when it's mathematically inferior.

Hamilton (2023) — the counter-punch

Eleven years later, the Southern Economic Journal paper quoted above used 2016 Survey of Consumer Finances data to quantify what the snowball costs. The extra-interest ranges — 1.8% to 4.3% per household, $46.2 to $53.9 billion in aggregate — are dramatic on their own. But the paper goes further:

That is: the snowball's extra cost is proportionally larger for lower-income and Black households, which can exacerbate racial and economic wealth gaps over time. This specific distributional finding appears in zero of the top 10 articles currently ranking for this keyword — which is one reason we wanted to include it here.

Amar et al. (2011) — "debt account aversion"

Duke's Dan Ariely co-authored a paper titled Winning the Battle but Losing the War: The Psychology of Debt Management (Journal of Marketing Research 48 Special Issue: S38-S50). Across four experiments, participants consistently paid down small debts first even when larger debts carried higher interest rates — a phenomenon the authors named "debt account aversion." The title captures the point: closing small accounts feels like winning, but the total-debt math can be getting worse.

Gathergood et al. (2019) — what Americans actually do

This American Economic Review paper (109(3): 844-875, also NBER w24161) may be the most surprising of the bunch:

Most American cardholders use neither snowball nor avalanche. They allocate payments proportionally to balance size — a strategy worse than either named method. In this context, Ramsey's advice to follow any rule is better than most people's actual behavior.

The scorecard

| Study | Finding | Implication for snowball |

|---|---|---|

| Gal & McShane 2012 | Account closures predict finishing debt repayment | Psychological effect is real |

| Amar et al. 2011 | People pay small balances first even when APRs differ | The behavioral bias is measurable |

| Hamilton 2023 | $46-54B per year in extra interest; falls hardest on low-income + Black households | Aggregate cost is substantial and unequally distributed |

| Gathergood et al. 2019 | Most cardholders balance-match (suboptimal) | A rule — any rule — beats the default |

Ramsey is half-right. Centering behavior and finish probability is the correct instinct. Dismissing avalanche entirely understates how much interest sophisticated borrowers can save.

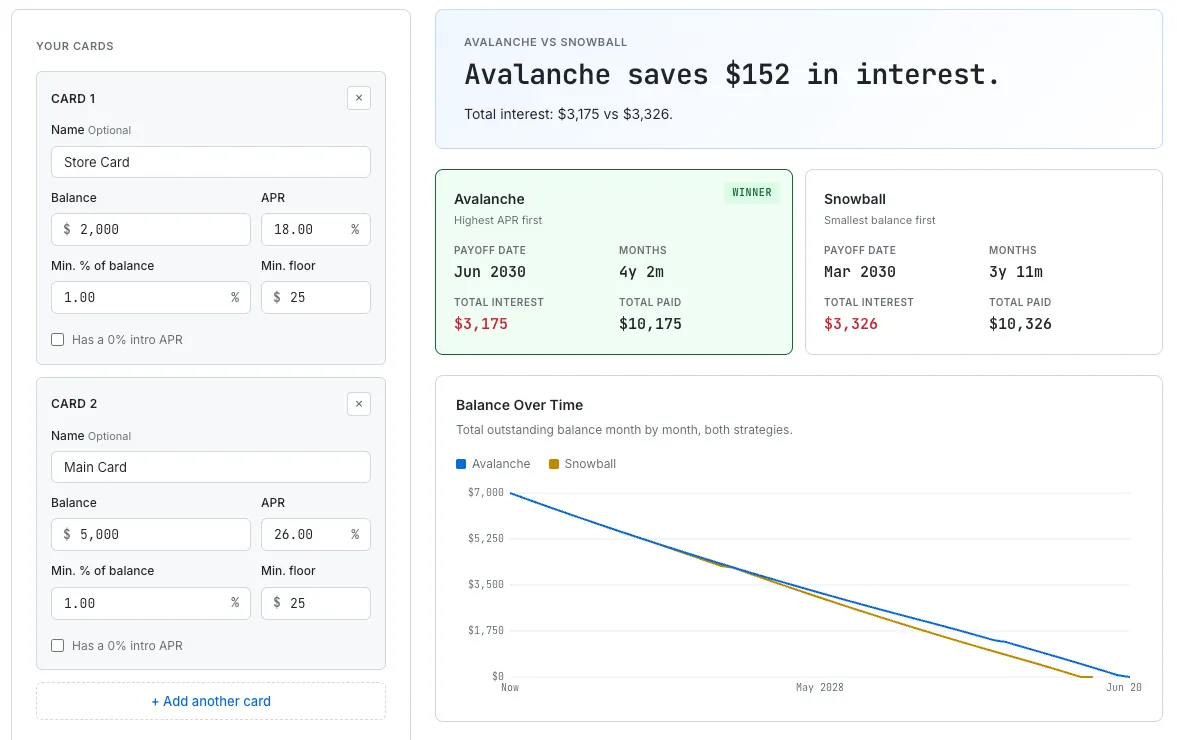

A Real Worked Example on Two Common Cards

Enough theory. Here are actual numbers from our Credit Card Payoff Calculator using its default two-card setup:

| Card | Balance | APR |

|---|---|---|

| Store Card | $2,000 | 18% |

| Main Card | $5,000 | 26% |

Adding $100/month extra on top of minimum payments, both strategies run in parallel produce:

| Method | Months to payoff | Total interest | Payoff order |

|---|---|---|---|

| Avalanche | 50 (4y 2m) | $3,175 | Main (40) → Store (50) |

| Snowball | 47 (3y 11m) | $3,326 | Store (18) → Main (47) |

| Difference | Snowball 3 months faster | Avalanche saves $152 | — |

Here's the twist: avalanche saves $152 in interest, but snowball finishes 3 months earlier. That's the opposite of what most articles tell you.

Why does this happen? When snowball pays off the smaller Store Card in month 18, its minimum payment (around $25-40) becomes freed cash that rolls into extra payments on the Main Card. Avalanche doesn't free that extra payment until month 40, when the Main Card is done — so the "rollover fuel" is delayed. On interest paid, avalanche still wins. On calendar time, snowball can win in multi-card scenarios.

How to Decide — a 4-Question Framework

Run these four questions in order:

Q1. Is your highest-APR card also your smallest-balance card?

→ Yes: both methods pick the same card first. No need to choose.

→ No: continue to Q2.

Q2. Is your APR spread narrow (e.g., all cards between 18% and 24%)?

→ Yes: the cost difference is small (typically $30-$300). Pick the method that motivates you.

→ No (wide APR spread, e.g., 15% vs 29%): continue to Q3.

Q3. Do you have a history of quitting financial plans partway through?

→ Yes: snowball. Momentum matters more than optimization.

→ No: continue to Q4.

Q4. Are you more motivated by numbers than feelings?

→ Yes: avalanche. Minimize total interest.

→ In-between: consider the hybrid approach below.

The most important rule: the method you actually finish beats the method that looks optimal on a spreadsheet. Gathergood et al. (2019) makes this the defining constraint — having a strategy beats the default behavior of balance-matching, regardless of which strategy you pick.

The Hybrid Strategy — Snowball First, Then Avalanche

A compromise widely taught by credit unions and financial counselors, even though it has not been formally tested in a peer-reviewed paper:

- Month 1: put all extra payment on the smallest-balance card.

- After the first card is paid off (usually within a few months), switch the target to the highest-APR remaining card.

- Continue with standard avalanche from there.

Advantages: you get the early psychological win of closing an account, then switch to the interest-minimizing strategy for the bulk of the payoff window.

Caveat: our Credit Card Payoff Calculator doesn't automatically simulate hybrid mode. But you can approximate it by running snowball until the first card is paid off, then switching to avalanche for the remaining balances. The results usually land between pure snowball and pure avalanche, closer to avalanche.

Frequently Asked Questions

Is debt snowball or avalanche better for paying off credit cards?

Mathematically, avalanche almost always wins — it minimizes total interest by attacking the highest-APR card first. But a 2012 Northwestern Kellogg study found that closing accounts is a stronger predictor of finishing debt repayment than the dollar size of the balance closed. For most households, the best method is the one they will actually complete, not the one that looks best on paper.

Does Dave Ramsey recommend the avalanche method?

No. Dave Ramsey teaches the snowball method exclusively through Financial Peace University. His reasoning is that personal finance is 80% behavior and 20% head knowledge. Ramsey's position has reached roughly 10 million FPU graduates but has drawn peer-reviewed academic criticism, most notably Hamilton (2023), who estimates the snowball costs US households $46 to $54 billion per year in extra interest.

Which method pays off debt faster in calendar time?

Avalanche almost always finishes sooner or in the same month as snowball. However, in certain multi-card scenarios, snowball can finish a few months earlier because paying off a small card first frees that card's minimum payment to roll into the next target. Our Credit Card Payoff Calculator shows this edge case on its default example — snowball finishes 3 months sooner while avalanche still saves $152 in interest.

How much more interest do you pay with the snowball method?

According to Hamilton (2023) in the Southern Economic Journal, the average US household using snowball instead of avalanche pays an additional 1.8% to 4.3% in total interest. Aggregated across all households, that represents $46.2 to $53.9 billion per year transferred from borrowers to lenders. The cost is proportionally higher for Black households and low-income households.

Can I combine the snowball and avalanche methods?

Yes. A common hybrid is to start with snowball for your first one or two cards to build momentum, then switch to avalanche for the rest. No peer-reviewed paper has formally tested this hybrid, but it is widely taught by credit unions and financial counselors as a way to capture both the motivational benefit and most of the interest savings.

Does paying off debt in this order affect my credit score?

Both methods eventually improve your score as balances drop. Snowball may give a slightly faster short-term score bump because FICO weighs per-account utilization — paying one card to zero quickly reduces that card's utilization to zero, while avalanche spreads the effect across cards. The difference is modest and temporary.

What if my smallest debt is also my highest-APR debt?

Then both methods recommend the same card first, and you do not need to choose. This is common with store credit cards, which often carry 26-29% APR alongside smaller balances, combined with larger mainstream cards at 18-22% APR. You are effectively running both methods at once.

How long does it take to pay off $10,000 in credit card debt?

At 22% APR with minimum payments only, roughly 24.6 years and $16,965 in interest. Adding $300 per month on top of the minimum cuts that to about 2.4 years and reduces total interest to $2,582. Use our Credit Card Payoff Calculator to run your exact scenario.

Bottom Line

Avalanche almost always saves interest. Snowball helps more people actually finish. The gap — averaging 1.8-4.3% extra interest per household, or $46-54 billion nationally — is real, and it falls hardest on the households that can least afford it. But a method you'll finish beats a method you won't.

The practical move: run your actual cards through a calculator first, so the math is a choice instead of an assumption. If the difference is $150 and you know yourself, pick snowball without guilt. If the difference is $3,000 and you know you'll stick with it, pick avalanche. Either way, pick something — because balance-matching is what most people do by default, and balance-matching loses on both counts.