Understanding Exchange Rates: A Traveler's Guide to Currency Conversion

From the mid-market rate to hidden airport fees, Dynamic Currency Conversion traps, and practical strategies to keep more of your money when traveling abroad.

There is a market where $9.6 trillion changes hands every single day. It's not the stock market. It's not real estate. It's the foreign exchange market (forex) — the largest financial market in the world (BIS, April 2025 Triennial Survey). The output of this massive market is the number you see on an ATM screen abroad — the exchange rate.

The problem is that most travelers lose money without realizing it because they don't understand how exchange rates work. Airport currency exchanges mark up the mid-market rate by 5–15%. Pressing "yes" when an overseas ATM asks "charge in your home currency?" adds another 5–8% in hidden fees. Factor in credit card foreign transaction fees, and you can lose $50–150 for every $1,000 you spend abroad.

This guide explains what exchange rates are, how they're determined, why they fluctuate, and — most importantly for travelers — how to minimize fees and get the best possible rate. Whether you're planning an overseas trip or sending money internationally, you'll walk away understanding exchange rates clearly.

What Is an Exchange Rate?

An exchange rate is the ratio at which one country's currency is exchanged for another. For example, if the USD/KRW rate is 1,350, that means 1 US dollar can buy 1,350 South Korean won.

The Mid-Market Rate vs. What You Actually Get

To understand exchange rates, you need to distinguish three key concepts.

The mid-market rate is the exact midpoint between the buy (bid) and sell (ask) prices in the interbank foreign exchange market. For example, if GBP/EUR has a bid of 1.1740 and an ask of 1.1744, the mid-market rate is 1.1742. This is also called the "real rate" or "interbank rate," and it's what Google and XE show you when you search for an exchange rate.

But the rate you actually receive is different. Banks, exchange bureaus, and card companies add a spread on top of the mid-market rate to earn their profit. The larger the spread, the more money you lose. Banks typically apply a 2–3% spread, while airport exchanges can charge 5–15%.

Fixed vs. Floating Exchange Rates

The world's exchange rate systems fall into two broad categories.

Fixed exchange rates are maintained when a central bank pegs its currency to another currency — usually the US dollar. The Hong Kong dollar (HKD) is fixed to the USD via a currency board, and the Saudi riyal (SAR) maintains a conventional peg to the USD.

Floating exchange rates are determined by market supply and demand. Most advanced economies — including the US, Eurozone, UK, Japan, and South Korea — use this system. The IMF classifies the exchange rate regimes of all 191 member countries annually. The recent trend is toward managed floats and soft pegs rather than fully free-floating rates.

How Are Exchange Rates Determined?

Under a floating exchange rate system, rates change almost constantly. Here are the key factors that drive them.

Supply and Demand

This is the most fundamental principle. When demand for a country's currency rises, its value appreciates; when demand falls, it depreciates. For example, when foreign tourists flock to Japan, increased demand for yen pushes its value upward.

Interest Rate Differentials

Currencies of countries with higher interest rates tend to strengthen, because investors move capital toward higher yields. A strategy that exploits this is the carry trade — borrowing in a low-interest-rate currency (e.g., Japanese yen at 0.75%) and investing in a high-interest-rate currency (e.g., US dollar), profiting from the rate differential.

Inflation and Purchasing Power Parity (PPP)

Currencies of countries with high inflation tend to weaken over the long term. The theory that formalizes this principle is Purchasing Power Parity (PPP) — the idea that a basket of goods should cost the same in any country when expressed in a common currency.

The most intuitive illustration of this theory is the Big Mac Index, published by The Economist since 1986. As of July 2025, a Big Mac costs $5.79 in the United States. In Switzerland it's about $8.70 (~50% higher — suggesting the Swiss franc is overvalued), while in Taiwan it's about $2.41 (~58% lower — suggesting the Taiwanese dollar is undervalued). It's an informal indicator, but it's remarkably useful for intuitively understanding relative currency values (The Economist — Big Mac Index data).

Trade Balances and the Current Account

Countries that export more than they import tend to see their currency appreciate, because foreign buyers need to purchase the exporting country's currency to pay for goods. Conversely, persistent current account deficits can weaken a currency. According to the IMF, large and sustained current account deficits increase the risk of sudden capital outflows and exchange rate crises.

Political Stability and Economic Performance

Political instability, policy uncertainty, and economic crises erode investor confidence, triggering capital flight and sharp currency declines. A textbook example: the British pound crashed to an all-time low after the UK government's "mini-budget" announcement in September 2022.

A Brief History of Exchange Rates

Today's exchange rate system wasn't built overnight. It's the product of 150 years of trial and error.

The Gold Standard Era (1870s–1914)

Under the gold standard, each country's currency was fixed to a specific amount of gold. After unified Germany adopted the gold standard in 1871, nearly every country in the world — except China and some Central American nations — was on the gold standard by 1900 (World Gold Council). The system guaranteed exchange rate stability, but collapsed with the outbreak of World War I in 1914 — as warring nations banned gold exports and suspended gold convertibility to finance the war effort.

The Bretton Woods System (1944–1971)

In July 1944, delegates from 44 nations gathered in Bretton Woods, New Hampshire, to design a new international monetary system. The core arrangement: the US dollar was pegged to gold at $35 per ounce, and all other currencies were pegged to the dollar. This conference also created the IMF and the World Bank.

The system was possible because the United States held roughly two-thirds of the world's gold reserves at the end of the war. But as the US share of global economic output declined — from about 40% in the 1960s to roughly 27% by the late 1970s — and Vietnam War spending and massive foreign aid pushed the volume of dollars in circulation well beyond US gold reserves, the system began to crack (Federal Reserve History).

The Nixon Shock (August 15, 1971)

President Nixon abruptly suspended the dollar's convertibility into gold. This was the "Nixon Shock" — effectively ending the Bretton Woods system. By March 1973, major countries had officially transitioned to floating exchange rates, the system we use today (U.S. State Department).

Key Events Since Then

The Plaza Accord (September 1985) — The US, Japan, the UK, France, and West Germany agreed at the Plaza Hotel in New York to deliberately weaken the US dollar through coordinated intervention. The dollar fell 40% over the following two years, and the resulting sharp yen appreciation contributed to Japan's asset bubble of the late 1980s.

The Asian Financial Crisis (July 1997) — Triggered when Thailand abandoned its dollar peg after exhausting its foreign reserves. The crisis spread to Malaysia, the Philippines, Indonesia, and South Korea. Nominal GDP per capita (in USD terms) dropped 43.2% in Indonesia, 21.2% in Thailand, and 18.5% in South Korea. The IMF provided rescue packages of approximately $17.2 billion for Thailand, $43 billion for Indonesia, and $58.4 billion for South Korea (Federal Reserve History).

The Euro (January 1, 1999) — Eleven EU member states — including Austria, Belgium, Finland, France, and Germany — introduced the euro as an electronic currency. Physical coins and banknotes entered circulation on January 1, 2002.

How Exchange Rate Fluctuations Affect Travelers

Exchange rates aren't a textbook abstraction — they directly determine how much your trip costs.

Real Cases Where Exchange Rates Changed Travel

The Japanese Yen (2022–2024) — The yen fell to a 38-year low of approximately 162 yen per dollar (161.96 in July 2024), turning Japan into a "country on sale" for foreign visitors. Tourist arrivals hit a record 30 million in the first ten months of 2024 (JNTO), and inbound tourism receipts reached an all-time high of 8.1 trillion yen for the year. Luxury goods were 20–30% cheaper than in visitors' home countries, fueling an explosion in "shopping tourism."

The British Pound (September 2022) — After the Truss government's mini-budget, the pound crashed to $1.03 ($1.0327) — its lowest level since 1971. British travelers saw their purchasing power abroad shrink overnight, while American tourists suddenly found the UK remarkably affordable.

The Turkish Lira (2021–2025) — The lira lost more than 80% of its value against the dollar (USD/TRY went from roughly 7.4 to 38–39), while inflation surged to 85.5% in October 2022. Initially, Turkey became an extremely cheap destination for foreigners, but rapid price increases quickly eroded that advantage — tourist-facing businesses began pricing in dollars or euros instead of lira.

How Much Do Exchange Rates Actually Move?

Major currency pairs like EUR/USD and USD/JPY typically fluctuate 1–3% per month under normal conditions. During high-volatility periods — interest rate hikes, geopolitical shocks — monthly moves can exceed 5%, and emerging market currencies (TRY, ARS) are far more volatile than that. The difference in exchange rates between a one-week trip and a one-month trip can amount to more than a night's hotel stay.

7 Hidden Fee Traps That Cost Travelers Money

The bigger problem isn't the exchange rate itself — it's the hidden fees. Here are the most common traps travelers fall into.

1. Airport currency exchanges. Convenient, but by far the most expensive option. They apply a 5–15% markup over the mid-market rate — even major chains like Travelex typically charge 8–9%. Exchanging $1,000 at an airport can cost you $50–150 in fees.

2. Dynamic Currency Conversion (DCC). When an overseas shop or ATM asks "Would you like to be charged in your home currency?" — always say no. If you say yes, the merchant applies their own unfavorable exchange rate. Research shows the average DCC markup is 5–8%, with documented cases reaching 12–18%. Combined with your card's foreign transaction fee, a single purchase can cost you up to 20% more.

3. Foreign transaction fees. Most credit cards charge 1–3% on every overseas purchase. This typically consists of a network fee (~1%, charged by Visa/Mastercard) plus an issuing bank fee (~2%).

4. Overseas ATM withdrawal fees. ATM operator fees ($3–5) plus your home bank's fee ($2–5) plus a percentage-based fee (1–3% of the withdrawal amount) all stack up. A single withdrawal can cost $10+ in fees alone. Standalone ATMs in tourist areas charge higher fees than bank-owned machines.

5. Hotel and tourist-area exchange booths. Tourist-area exchange markup ranges from 2–10%, with hotel-based exchanges reaching 15% or more. One hotel chain was documented applying a double conversion (local → USD → local) resulting in an effective markup of over 30%.

6. Frequent small exchanges. When flat per-transaction fees apply, exchanging small amounts repeatedly causes the effective fee percentage to skyrocket. Exchange the amount you need in fewer, larger transactions whenever possible.

7. Exchanging without checking the rate. A quick search for "USD to THB" on Google shows you the mid-market rate instantly. Without knowing this benchmark, you have no way to judge whether the rate an exchange booth offers is good or bad.

A Smart Traveler's Guide to Currency Conversion

Now that you know the traps, here are practical strategies to avoid them.

Use a Card with No Foreign Transaction Fees

As of 2026, approximately 30% of credit card products charge no foreign transaction fees. Capital One charges zero FTF on all its cards, and Chase Sapphire, Bank of America Travel Rewards, and many others follow suit. This single card saves you up to 3% on every overseas purchase.

Always Choose Local Currency

When a shop, restaurant, or ATM asks "charge in your home currency?" — always select local currency. Your bank or card issuer's exchange rate (mid-market rate + 1–2%) is always better than a DCC rate (mid-market rate + 5–18%).

ATM Strategy

Use bank-owned ATMs (HSBC, Citi, major local banks) rather than standalone machines in tourist areas, hotels, or convenience stores. Withdraw larger amounts less frequently to minimize per-transaction flat fees — but don't withdraw more than you'll actually need. ATMs can also offer DCC, so always decline the home-currency option.

Cash vs. Card Ratio

Experts recommend carrying 20–30% of your travel budget in cash, with the rest on cards. Cash is needed for tips, local markets, small shops, and public transit where cards aren't accepted. In developed countries, you can go 70–80% card. In rural areas or developing countries, increase your cash ratio to 50%+.

Use Fintech Services

Wise (formerly TransferWise) charges a minimal fee starting at 0.41% on top of the mid-market rate and supports 40+ currencies. Revolut applies the mid-market rate within monthly limits (Standard plan: 1% weekend markup; Premium and above: no weekend markup) and offers free ATM withdrawals within monthly limits. Traditional banks charge roughly 5% per transaction (rate markup + fees combined) — a massive difference (Wise).

Making Currency Conversion Easy While Traveling

Once you understand how exchange rates work and how to avoid hidden fees, the most important thing in practice is instantly converting local prices to your home currency. Is a 550-baht pair of pants at a Thai market expensive? How much is a 250-yen rice ball at a Japanese convenience store? You need to be able to judge immediately.

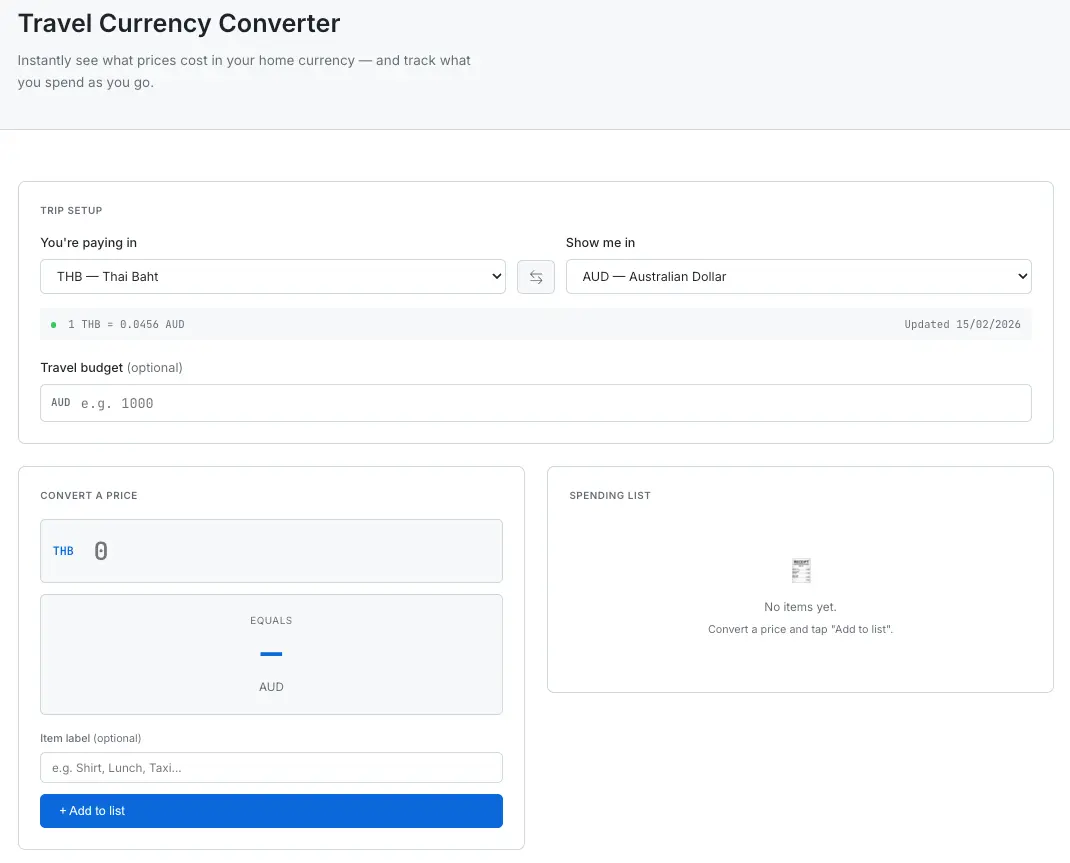

SudoTool's Travel Currency Converter was built to solve exactly this problem. Enter a local price and see the equivalent in your home currency instantly. Label each item ("shirt," "taxi," "dinner") and add it to a running spending list that tracks your total expenses in real time. Set a budget and see your remaining balance color-coded — green (on track), yellow (under 20% remaining), red (over budget). It supports 160+ currencies, and all data is stored in your browser — nothing is sent to any server.

SudoTool Travel Currency Converter — convert prices instantly, track spending, and stay within budget.

Frequently Asked Questions

What is an exchange rate?

An exchange rate is the ratio at which one currency is exchanged for another. For example, USD/KRW = 1,350 means 1 US dollar equals 1,350 Korean won. Exchange rates fluctuate almost constantly based on supply and demand in the foreign exchange market.

What is the mid-market rate?

The mid-market rate is the exact midpoint between the buy and sell prices in the interbank foreign exchange market. It's what Google and XE show you — also called the "real rate." Banks and exchange bureaus add a markup on top of this, so the rate you actually receive is always less favorable.

Why are airport exchanges so expensive?

Airport exchanges charge 5–15% markups over the mid-market rate due to high rent, 24/7 operating costs, and the knowledge that travelers have few alternatives. It's almost always better to exchange at a local bank before departure or use a bank-owned ATM at your destination.

What is Dynamic Currency Conversion (DCC)?

DCC is when an overseas merchant or ATM offers to charge you in your home currency instead of local currency. It sounds convenient, but the merchant applies their own unfavorable exchange rate — typically a 5–8% markup on average. Always choose to be charged in the local currency.

What is the Big Mac Index?

An informal purchasing power parity indicator published by The Economist since 1986. It compares the price of a Big Mac across countries in US dollar terms to show whether currencies are overvalued or undervalued. As of July 2025, Switzerland is the most overvalued (~50% above the US price) and Taiwan the most undervalued (~58% below).

What's the right cash-to-card ratio for international travel?

Experts generally recommend 20–30% cash and 70–80% on a no-foreign-transaction-fee card. In developed countries you can lean heavily on cards, but in rural areas or developing countries you should carry 50%+ in cash for places that don't accept cards.

Which is better for travel — Wise or Revolut?

Both offer dramatically better rates than traditional banks. Wise charges a transparent fee starting at 0.41% on top of the mid-market rate. Revolut applies the mid-market rate within monthly limits (Standard plan: 1% weekend markup; Premium+: no weekend markup). Wise is generally better for frequent, high-volume travelers; Revolut offers more features (stocks, crypto) beyond currency exchange.

How much can exchange rate fluctuations affect travel costs?

Major currency pairs fluctuate 1–3% per month under normal conditions and 5%+ during crises. When the Japanese yen hit a 38-year low in 2024, inbound tourism receipts reached an all-time high of 8.1 trillion yen. Exchange rate moves can easily amount to more than a night's hotel stay.

Exchange Rates — Now You're in Control

Exchange rates are complex numbers fluctuating every second in a $9.6 trillion market. But as a traveler, you only need to remember three things:

Use the mid-market rate as your benchmark — check Google before you exchange, and compare the markup. Always pay in local currency — the "convenience" of DCC costs 5–18%. Know your fees in advance — a no-foreign-transaction-fee card, bank-owned ATMs, and the right cash-to-card ratio are what matter most.

If you want to instantly convert local prices and track your spending while traveling, try SudoTool's Travel Currency Converter.

Curious about how this tool was built? Read how we built a browser-based travel currency converter — the design decisions, technical trade-offs, and lessons learned along the way.